To be sure, the office market is in bad shape throughout much of the country. According to Cushman & Wakefield, a respected commercial real estate analytics firm, the national office vacancy rate reached 18.6 percent in the first quarter of 2023. This is up from roughly 13 percent in the first quarter of 2020. Office space absorption was a negative 32.2 million square feet and has been negative for 11 of the past 12 quarters. [1] An estimated 7 percent of office buildings are at least 50 percent vacant, leading some property owners to default on their commercial mortgages and essentially give the keys back to the bank. [2]

How Bad Is It Really?

The answer is pretty bad, but not end-of-the-world bad. The key point to understand is that the current struggles of the office market are not due primarily to an economic recession or rising interest rates. All real estate markets tend to be cyclical to some degree, but this is not the traditional trough in the office market cycle. There have been some fundamental changes that have caused vacancy rates to soar and those changes will not go away with the next economic recovery. Yes, the office market will eventually rebound but it will end up being different and that difference needs to be understood by both developers and city officials.

As noted above, the national office vacancy rate is 18.6 percent, but the poster child for office problems has been San Francisco which has a vacancy rate of 24.8 percent and has experienced a net space absorption over the past year of negative 3.7 million square feet. This historically bad performance is partly due to the tech industry which during the early parts of the pandemic went on a crazy hiring spree and corresponding scramble for new office space. Those same tech firms are rapidly unwinding that strategy and massive layoffs, combined with the national trend of remote work, have caused office demand to plummet.

But the problem is not just in San Francisco or other tech hubs. Office vacancy rates are much higher than normal in many cities across the county, including several in the midwest. Cities like Chicago (23.7), Minneapolis (25.1), Columbus (26.7) and Kansas City (21.1) all have vacancy rates over 20 percent and cutbacks in the tech industry are not to blame. It is also important to point out that vacancy rate averages can mask a fair amount of variability from market to market, and even within a market area. Of the roughly 90 markets that Cushman & Wakefield track, 17 have vacancy rates under 10 percent. [1]

Despite the occasional bright spot, the office market in general is not performing well in most major cities and the primary culprit is the refusal of workers to return to pre-pandemic patterns of work. The pandemic forced people to work from home and while there were problems to overcome, many people found they preferred it to working in the office. I’m not going to rehash the pros and cons of this trend here, but simply remark that despite pressure from bosses to return to the office full-time, the workforce has been adamantly in favor of retaining at least some work-from-home options. The compromise that has been struck is known as a hybrid work schedule which generally means two to three days in the office each week and the remainder as remote work. For reasons I will outline later in this post, this trend is not likely to change anytime soon, if ever.

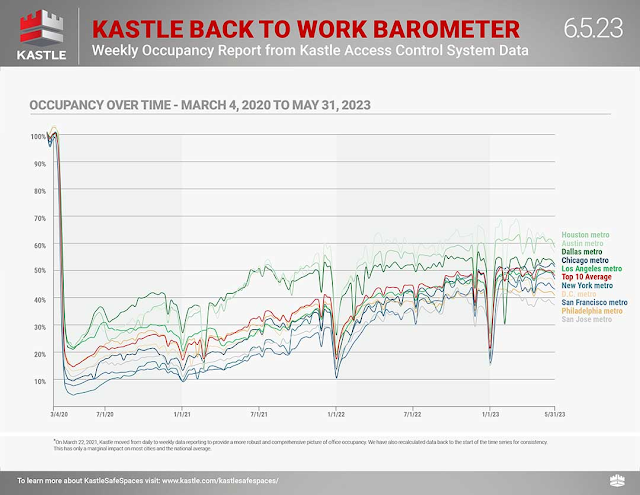

Kastle Systems is a provider of corporate security systems, including the hardware and software used to allow employees to enter their place of work (typically by swiping an access card to unlock entry doors). Kastle collects data on each “swipe” and has parlayed this information into an indicator of how quickly office employees are returning to work and what their work schedule is like. This is an admittedly small data sample (300,000 workers in 10 cities) but it has proven to be relatively accurate when compared with other data sources and it provides real time data that is difficult to find anywhere else. The result is a measure of office utilization that is distinct from, although related to, office vacancy rates.

What Kastle has found is that workers are in the office roughly half as much as they were prior to the pandemic. This number is slowly creeping upward, but it is not showing signs of returning to anything close to pre-pandemic levels. In fact, for most of 2023 this metric has been basically flat or slightly declining. Tuesdays are the most popular day to be in the office (an average occupancy equal to 57.6% of pre-pandemic levels) while Friday is clearly the least favorite day to be in the office (32.4% of pre-pandemic levels).

|

| Source: Kastle Systems, Inc. |

Regardless of what the exact number is, office utilization is low and that is causing companies to rethink their office space needs. Companies are canceling plans to build bigger buildings or corporate campuses, subleasing space that is suddenly unnecessary, and either dropping leases that are up for renewal or re-signing for less floor area. One of the reasons this is not a short-term trend is that companies can save considerable money with work-from-home. If companies can reduce their office footprint, they are essentially trading expensive leased space in an office building for free space in each employee’s home. By one estimate, that could add up to annual savings of $11,000 per employee. [3]

Consequently, office building owners are facing higher vacancies and lower revenue streams. Lower revenue streams eventually translate into lower building valuations and sets up the possibility of foreclosures if revenue no longer covers debt service costs. The one bright spot has been that Asking Rent has increased throughout the pandemic and now averages just over $37 per square foot. [1] The general consensus is that this represents a “flight to quality” as companies trade the money they save by reducing leased square footage into somewhat nicer space with better amenities. Consequently, the highest quality buildings tend to be the ones that are doing the best. The older, Class B and C buildings tend to be struggling the most.

A Brief History

Before leaping into the future, a look at how we arrived at our current predicament will hopefully provide some context for what I think is to come. The problems we face are the result of well established trends, not of occurrences that came out of the blue. The pandemic forced changes to occur rapidly, but they likely would have happened eventually even if the pandemic had never occurred. The future, in turn, will be based on trends that are still playing out, not on some presumed return to “normal” that is based more on nostalgia than reality.

In my opinion, the roots of the current office market goes back at least 50 years to the transition from an industrial economy to a knowledge economy. America exported manufacturing jobs to low-wage countries and compensated by taking advantage of our substantial lead in college graduates and computers. American firms became the designers, marketers and financiers for much of the world. Jobs were created that had never existed before, and many others mutated and multiplied.

These new jobs needed a new work environment. Big office buildings in big cities became the answer. And while the cities with the most money, talent and computing sophistication were the big winners, virtually every city benefitted to some degree. Downtowns and office parks saw new buildings being built like never before, and incoming workers created an urban resurgence. The losers were rural areas that lost population in a self-reinforcing cycle of decline and the traditional industrial cities which saw their factories shuttered and their blue-collar workforce become largely unemployable.

The evolution of computers and networks. Much of what has driven progress in the knowledge economy has been the parallel progress in computers and computer networking. Mainframe computing marked the beginning of the knowledge economy, but that evolved fairly quickly into distributed computing on Unix workstations and then on personal computers. That led to personal computers linked together on local area networks, followed by client-server computing which combined software on personal computers with high-powered databases on centralized servers. Each step multiplied the productivity of individual workers and expanded the scope of problems that could be solved.

Eventually, local networks were connected to similar networks across the country or around the world leading to what we currently refer to as the internet. It is now easier to browse for information on the internet than it is to pull a book off a shelf and turn to the correct page. The power of internet computing resulted in nearly all software and data being moved to large server farms located in remote facilities that have little physical proximity to the average worker. This disconnect between workers and their data became so confusing to explain that it was sometimes diagrammed as a “cloud” of data servers that resided at some unspecified location.

This so-called “cloud computing” is now ubiquitous. White collar professionals used to come into the office in order to use locally stored data to produce paper reports for their colleagues and customers. Now they spend their day using browser-based applications that access data stored at facilities that have nothing to do with their office location. Even personal interactions, whether they be with a co-worker on the next floor or a client in a different city, are generally computer based because that is where all the information resides. Workers only occasionally need face-to-face meetings or access to the printers, copiers and other devices that offices provide. Now that the majority of people have high-speed internet access at home, there is virtually no reason for them to come into the office to complete the bulk of their work. Working on a laptop in an office cubicle offers no clear advantage compared with using the same laptop at home.

The battle for brain power. If the industrial economy was about using machines to multiply the muscle power of workers making goods, the knowledge economy is about using computers to multiply the brain power of workers implementing ideas and completing transactions. Assembling the brightest minds became the path to corporate success.

For the first few decades, computers churned through data and automated routine tasks, but the most productive brainstorming and decision making took place face to face. This meant that having a lot of brain power at a single location was advantageous, particularly if that location was close to the offices of the biggest customers. Consequently, office buildings got bigger and more densely packed into big city business districts. Attracting talent was not only about pay, it was also about the prestige of working in a modern skyscraper at a prominent location near other major players in the industry.

Downtowns which had previously contained a mixture of office, retail and industrial buildings became heavily skewed toward office development. Land for office buildings became so valuable that few other uses could compete, leading retailers to move to outlying shopping centers and manufacturers to move to industrial parks with rail and highway access. This singular focus led to several dysfunctional characteristics. Commutes became time-consuming, stressful and expensive because everyone arrived and left at the same time. Rents became exorbitantly high and public spaces became too crowded during the day and nearly deserted at night and on weekends.

As a result, second-tier companies and employees left downtowns for suburban office parks that offered lower rents, free parking, and lush landscaping. Commuting was not necessarily less expensive or time-consuming, however, because their peripheral location meant that mass transit was rarely an option and urban ring roads quickly became just as congested as the roads leading to downtown. Still, suburban office parks were touted as a new way to attract high quality employees that were burned out on downtown locations.

Fast forward to current times when a new generation of workers is shifting the battleground for top level talent. Millennials and Gen-Z workers are generally not impressed by the prestige of a downtown location and are bored by the suburban office parks where Applebee’s is the leading lunch venue. The new generations take full advantage of technology to blend their work and personal lives. Above almost everything else, they value scheduling flexibility and proximity to the important people and places in their lives. A job with work-from-home options is not a perk that will land the best and brightest, it is a minimum requirement for any job they will seriously consider.

At the same time, there are additional factors acting to reduce the number of employees that need to be housed in high-prestige, high-dollar locations. Office automation, for example, continues to enhance professional productivity and lessen the need for support staff. The off-shoring of white collar work continues to gain popularity much like the off-shoring of manufacturing 30 years ago. Finally, the rise of artificial intelligence will accelerate the office automation trend and reduce the need for certain white collar jobs. Yes, new kinds of jobs will be created by the boom in AI, but they will likely not be housed in downtown office buildings.

The Ripple Effects

The bottom line is that the office market is fundamentally different than it was just 5 or 10 years ago and the effects will ripple throughout both the commercial real estate industry and municipal budgets. This is not a temporary “glut” of office space caused by overbuilding. In fact, the pipeline of new office construction is down significantly in 2023 and is likely to drop further in 2024. [1] Nor can vacancy rates be blamed on an economic recession with high unemployment. Hiring has been booming lately and unemployment is at near-record lows. Office demand should be growing, not shrinking. If rising interest rates do cause a significant recession as some have predicted, then the office market will fall even further into disarray than it is now.

Falling valuations. Building owners are being hit by a double-whammy of rapidly falling occupancy rates and rapidly rising interest rates at the same time. Both factors act to reduce the value of office buildings and building owners are feeling the pinch. The actual impact will vary from building to building, but drops of 20 to 30 percent will not be uncommon. At the extreme, some building owners will owe more on their mortgages than their building is worth. Hence, the beginning of what could be a significant trend in office foreclosures. [4]

Tightening financial options. The commercial real estate market has $1.5 trillion in debt coming due before the end of 2025. This debt is secured by a portfolio of office, retail, industrial and multi-family properties that may not be worth what they were five or ten years ago when the loans were made. [5] Office buildings represent only about a third of the commercial real estate market and the other sectors are doing somewhat better, but that is still a lot of refinancing that will need to take place at a time when most lenders are skittish, particularly of holding office buildings as collateral. Many owners will struggle to find financing options that they can afford.

Bank failures. A lot of the commercial debt that needs to be refinanced is held by regional banks that have problems of their own. Many depositors are pulling money out of banks because higher returns are available elsewhere and many banks own 10-year treasuries that are worth less than face value due to rising interest rates. Banks that also face rising delinquencies on office building loans could join the list of recent bank failures. Banks are generally in much better shape than they were during the 2008 housing crisis, but that could change if the office market really goes south.

Retail and service closures. The lack of office workers, particularly in downtown areas, is causing many restaurants, bars and service businesses to close down due to falling foot traffic leading to falling revenue. Consequently, retail space on the ground level of many office buildings is just as vacant as the office space on the upper floors. This is having a negative impact on the perceived vibrancy and safety of some downtown areas.

Dropping municipal revenues. Falling office valuations and vacant retail space has the potential to put a dent into both property tax and sales tax collections for cities and other governmental entities supported by those taxes. So far, the impact has been fairly muted but in a year or two that could change. Governments that have grown used to rising revenues due to rising property values could be in for a shock if that reverses.

Although all of these ripple effects are real, they are probably not as catastrophic as some analysts have forecast. Despite rising interest rates and the possibility of a recession, the national economy has been remarkably resilient. In addition, changes that followed the 2008 housing meltdown have left the real estate industry in a much more stable position. So while there will undoubtedly be pain, the sky isn’t falling quite yet.

Still, office developers, lenders and city officials need to be planning for change because the future of the office market will be different than the past. What might those changes look like? Tune into Part 2 next month!

Notes:

David Smith; “Marketbeats, U.S. National Office Statistics, Q1 2023”; Cushman & Wakefield; April, 2023; https://www.cushmanwakefield.com/en/united-states/insights/us-marketbeats/us-office-marketbeat-reports

Kastle Systems; “Back to Work Barometers”; May 2023; https://www.kastle.com/safety-wellness/getting-america-back-to-work/

Michael Tedder; “Here’s How Much Companies Can Save With Work From Home”; TheStreet.com; March 2022; https://www.thestreet.com/investing/heres-how-much-companies-can-save-with-work-from-home

Jack Witthaus; “Downtown in Distress: Los Angeles Signals Why Nation’s Office Space Headaches Could Last for Years”; CoStar; March 2023; https://www.costar.com/article/531623023/downtown-in-distress-los-angeles-signals-why-nations-office-space-headaches-could-last-for-years

Henry Grabar; “The Ticking Time Bomb in America’s Downtowns”; Slate; May 2023; https://slate.com/business/2023/05/downtown-real-estate-office-rent-vacancies-debt-commercial-reuse-conversions.html

Excellent and informative post this topic is very relevant for many people dealing with tax concerns. IRS issues and tax debt can quickly become overwhelming without proper support. At NasirCPA Tax Debt Solvers, we help taxpayers understand their options and find clear, practical solutions. Anyone looking for trusted tax relief guidance is welcome to visit our website: Payroll Taxes

ReplyDelete